India has emerged as a global powerhouse in the dairy industry, boasting a remarkable journey from a milk-deficient nation to the world’s largest producer of milk and milk products. The dairy sector has played a pivotal role in the country’s agricultural and rural economy, providing livelihood opportunities to millions of farmers and contributing significantly to the overall GDP. This article delves into the nuances of India’s dairy industry, shedding light on its evolution, current landscape, consumption patterns, government initiatives, and emerging investment opportunities.

The Evolution of India’s Dairy Industry:

Post-independence, India faced a dire situation with declining milk production and per capita availability. However, the implementation of Operation Flood, a dairy development program initiated in 1970, laid the foundation for a nationwide milk grid, connecting rural milk producers with urban consumers.

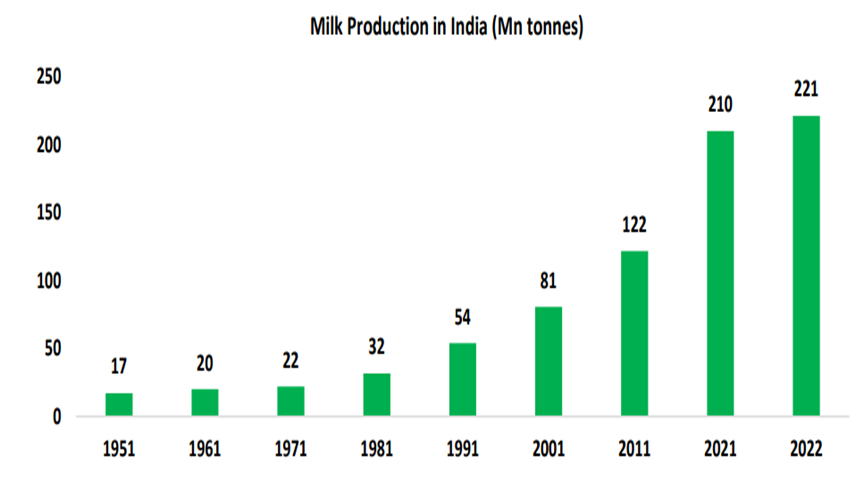

This transformative initiative paved the way for a remarkable surge in milk production, increasing from 22 million tonnes in 1970–71 to a staggering 220 million tonnes in 2022–23.

Consequently, the per capita milk availability witnessed a significant rise, from 112 grams per day in 1970–71 to an impressive 446 grams per day in 2022.

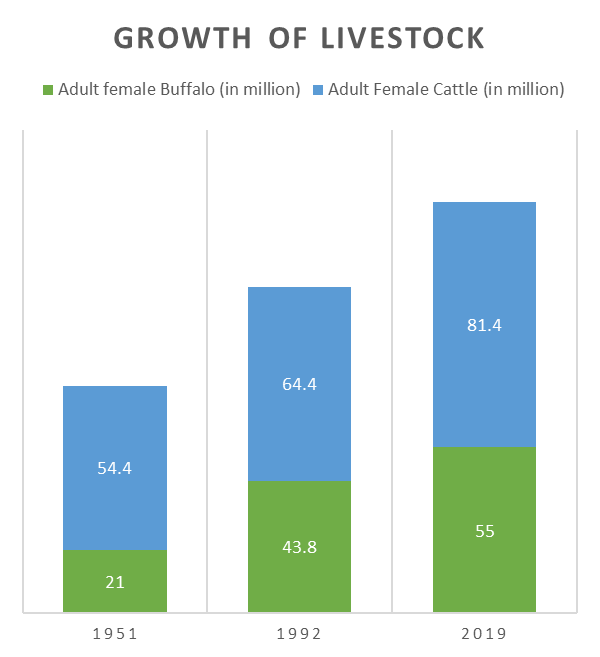

This growth can be attributed to the steady increase in the cattle and buffalo population, with adult female buffaloes increasing from 21 million in 1951 to 55 million in 2019, and adult female cattle growing from 54.4 million in 1951 to 81.4 million in 2019.

Milk Consumption Landscape:

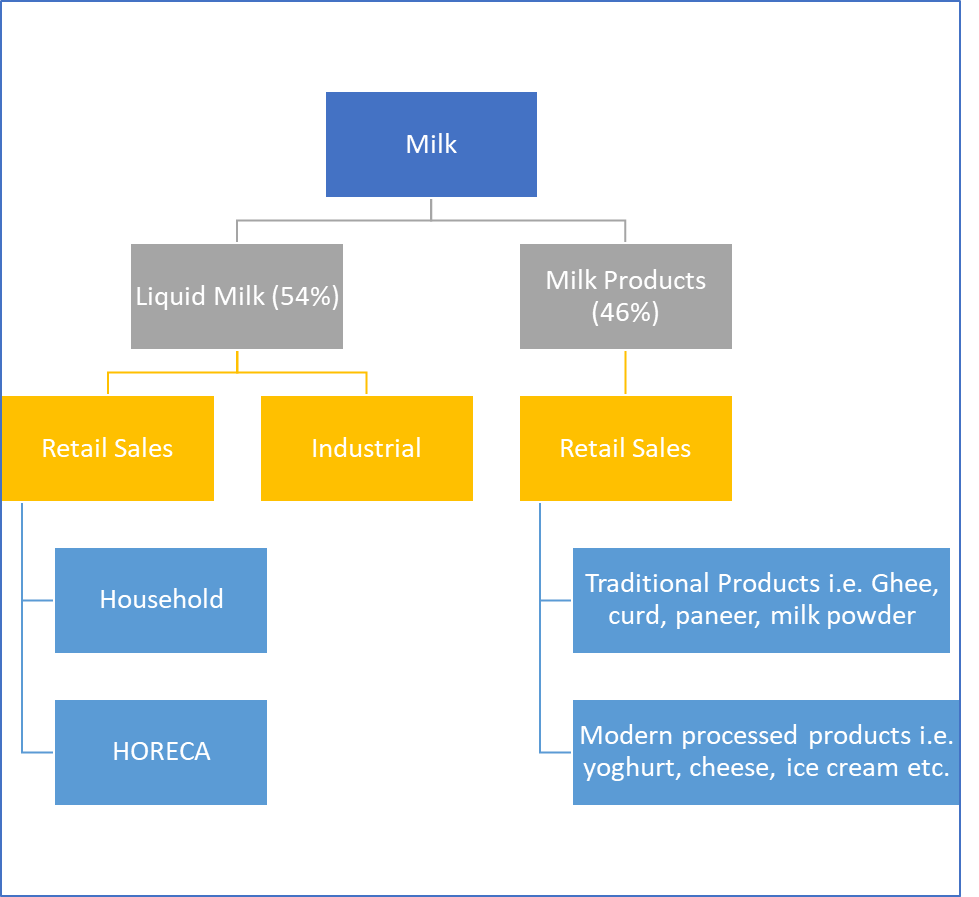

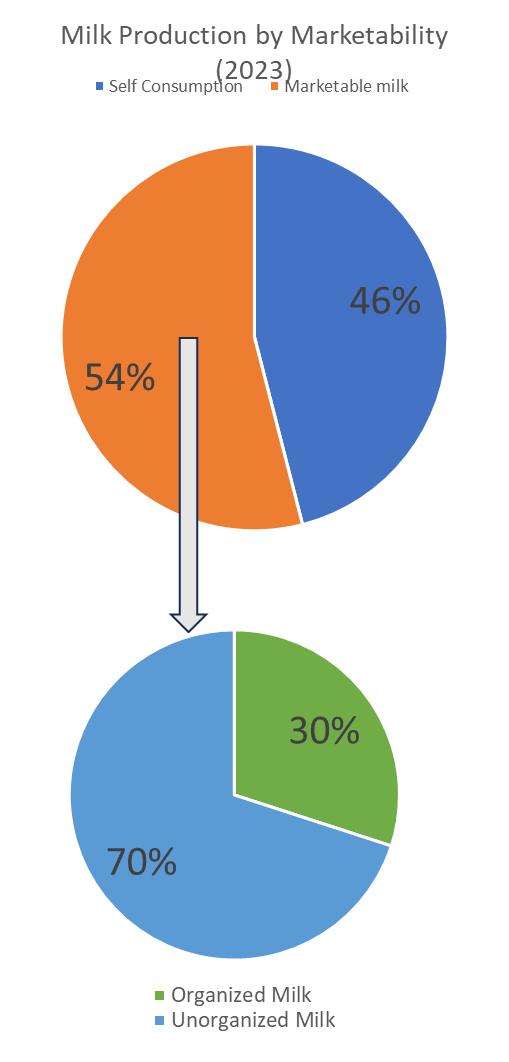

The Indian dairy market is segmented into two broad categories: liquid milk (54%) and milk products (46%). Liquid milk dominates the market, with a significant portion (70%) being sold through the unorganized sector due to localized sourcing and delivery. The organized segment is primarily controlled by cooperatives, with private players focusing more on modern processed products.

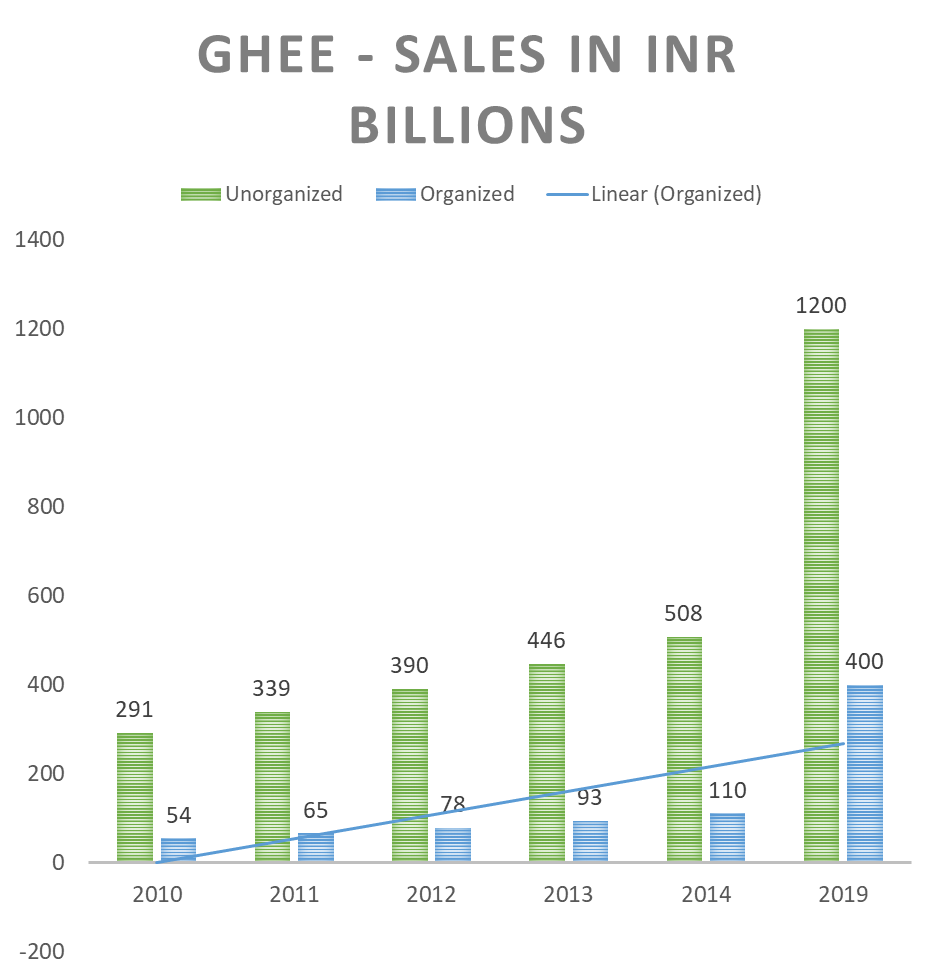

Traditional dairy products, such as ghee, curd, paneer, and milk powder, hold cultural significance and account for a substantial share of the market. However, emerging categories like cheese, flavored milk, and yogurt are witnessing remarkable growth, driven by changing consumer preferences, health consciousness, and the influence of western cuisines.

Cheese, in particular, stands out as one of the fastest-growing segments, with an expected CAGR of 21%+ between 2023 and 2032.

The per capita consumption of cheese in India, currently at 200 grams, is significantly lower than the global average of 7 kilograms, indicating ample growth potential, especially in urban areas where consumption is higher at 700 grams per capita.

The Rise of Alternate Milk:

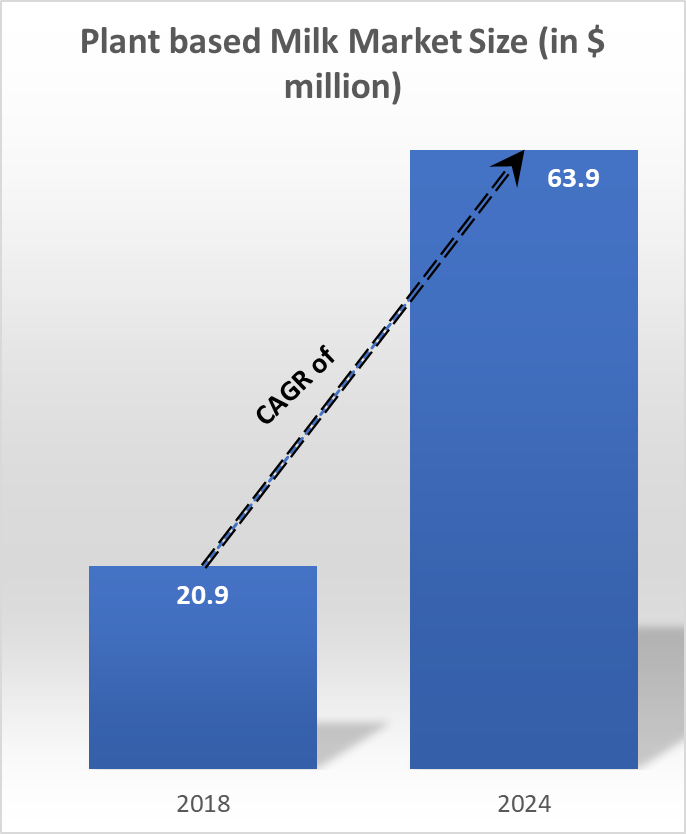

While dairy milk remains the predominant choice, the plant-based milk market in India is gaining traction. Valued at $20.9 million in 2018, it is projected to grow at a CAGR of 20.7% to reach $63.9 million by 2024. Soy milk, almond milk, and oats milk are the major types of plant-based milk sold in India, fueled by factors such as health consciousness, changing lifestyles, increasing demand for low-fat milk beverages, veganism, lactose intolerance, and environmental concerns.

Supply Chain and Infrastructure:

The dairy supply chain in India is complex, involving numerous stakeholders from cattle rearing and village-level collection to processing, distribution, and retail channels. Cooperatives play a crucial role in the sourcing and distribution of fresh liquid milk and traditional products, while private players dominate the value-added segment.

To strengthen the dairy infrastructure, the Indian government has launched several initiatives, including the Dairy Processing and Infrastructure Fund, Animal Husbandry Infrastructure Fund, National Program for Dairy Development, Pradhan Mantri Kisan Sampada Yojna, National Livestock Mission, and Rashtriya Gokul Mission. These programs aim to improve dairy processing capabilities, enhance animal productivity, and bolster the overall supply chain.

Emerging Investment Opportunities:

The Indian dairy industry presents a plethora of investment opportunities, driven by growing demand, changing consumer preferences, and untapped potential. Some promising areas include:

1. Dairy Financing: With over 100 million small-marginal farmers relying on informal sources for financing at high-interest rates, there is a significant opportunity for organized financing solutions tailored to their needs.

2. Traceable By-products (Cheese & Yogurt): As health awareness increases, demand for premium, traceable, and consistent quality cheese and yogurt brands is on the rise, creating opportunities for established players and newcomers alike.

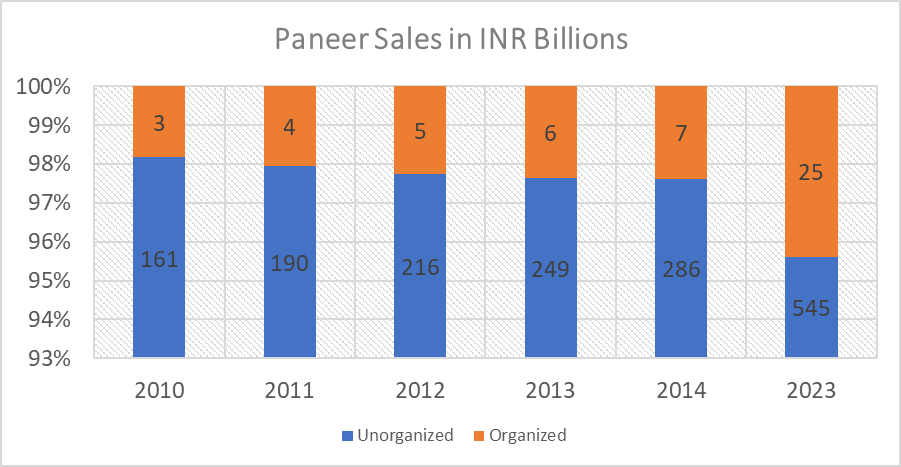

3. Paneer: Despite being a large category, the paneer market lacks established brands, leaving room for the creation of a national brand offering consistent taste and quality.

4. Whey Protein: With the protein supplements market valued at $4 billion and growing, and whey protein commanding a 50% market share, there is a significant opportunity for local brands to enter and capture a share of this lucrative segment.

Industry Insights and Challenges:

While the Indian dairy industry has witnessed remarkable growth, several challenges persist. The milk yield of Indian cows, at 4.87 kg, is only two-thirds of the global average of 7.2 kg, indicating a need for improved productivity. Additionally, the country faces a shortage of veterinarians, with only 63,000 registered professionals against a requirement of 110,000 to 120,000.

Adulteration remains a significant issue, particularly in the unorganized sector, necessitating stringent quality control measures and consumer awareness campaigns. Furthermore, the distribution of milk production across India varies, with indigenous buffaloes and crossbred cows contributing the highest shares of 31.94% and 29.81%, respectively.

Competitive Landscape:

The Indian dairy market is highly fragmented, with a diverse range of players operating at regional and national levels. While cooperatives dominate the liquid milk segment, private players have made significant inroads in value-added and processed dairy products. The competitive landscape is characterized by a mix of regional operations, pan-India operations, and product diversification strategies.

The Indian dairy industry has undergone a remarkable transformation, evolving from a milk-deficient nation to a global powerhouse. With its rich cultural heritage, growing demand, and strategic government initiatives, the sector holds immense potential for further growth and investment opportunities. However, addressing challenges such as productivity, infrastructure, and adulteration will be crucial for sustaining the industry’s momentum and ensuring a secure future for India’s dairy farming community.

As consumers become increasingly health-conscious and demand high-quality, traceable dairy products, the industry must adapt and innovate to meet these evolving needs. By leveraging technology, fostering collaborations, and implementing sustainable practices, the Indian dairy industry can pave the way for a future where nutritious dairy products are accessible to all, while contributing to the nation’s economic growth and rural development.

Blogs:-RSN